All Categories

Featured

Table of Contents

- – What is the best Legacy Planning option?

- – What types of Living Benefits are available?

- – How long does Wealth Transfer Plans coverage ...

- – How can Universal Life Insurance protect my f...

- – Whole Life Insurance

- – What happens if I don’t have Wealth Transfer...

- – How do I get Protection Plans?

- – Why should I have Riders?

- – Who has the best customer service for Policy...

- – What should I know before getting Estate Pla...

Juvenile insurance may be sold with a payor advantage cyclist, which gives for forgoing future premiums on the child's plan in the event of the death of the individual that pays the premium. Senior life insurance policy, sometimes described as graded fatality advantage plans, provides eligible older applicants with very little whole life protection without a medical exam.

These plans are usually much more expensive than a totally underwritten plan if the individual certifies as a standard risk. This type of coverage is for a little face amount, normally acquired to pay the funeral expenses of the guaranteed.

These plans can be a financial resource you can make use of if you're identified with a covered health problem that's thought about chronic, essential, or incurable. Life insurance policy policies fall into 2 classifications: term and long-term.

In addition, a section of the costs you pay right into your whole life policy builds money value over time. Some insurance policy companies provide tiny whole life plans, often referred to as.

What is the best Legacy Planning option?

Today, the price of an average term life insurance coverage for a healthy and balanced 30-year-old is approximated to be around $160 each year just $13 a month. 1While there are a great deal of variables when it concerns just how much you'll spend for life insurance (plan type, benefit quantity, your occupation, and so on), a policy is likely to be a lot cheaper the more youthful and much healthier you are at the time you buy it.

Beneficiaries can typically receive their money by check or electronic transfer. On top of that, they can likewise pick how much cash to get. They can obtain all the cash as a swelling sum, by means of an installation or annuity strategy, or a maintained property account (where the insurance coverage business acts as the bank and allows a recipient to create checks against the balance).3 At Freedom Mutual, we understand that the decision to get life insurance policy is a vital one.

What types of Living Benefits are available?

Every effort has actually been made to guarantee this information is existing and correct. Details on this web page does not guarantee registration, benefits and/or the capability to make modifications to your advantages.

Age decrease will use during the pay duration including the protected person's relevant birthday celebration. VGTLI Age Reduction Age of Worker Amount of Insurance 65 65% 70 40% 75 28% 80 20% Recipients are the individual(s) assigned to be paid life insurance policy benefits upon your death. Recipients for VGTLI coincide as for GTLI.

How long does Wealth Transfer Plans coverage last?

This advantage might be proceeded up until age 70. You have 30 days from your retired life day to elect this insurance coverage utilizing one of the two choices listed below.

Total and send the Retiree Team Term Life Enrollment create. The completed kind must be mailed to the address kept in mind on the type. Subsequent quarterly premiums in the amount of $69 are due on the initial day of the complying with months: January, April, July and October. A premium due notification will certainly be sent out to you around thirty day before the next due day.

You have the choice to pay online utilizing an eCheck or credit/debit card. Please note that service fee may apply. You additionally have the alternative to send by mail a check or money order to the below address: The Ohio State UniversityAccounts ReceivablePO Box 182905Columbus, OH 43218-2905 Costs rates for this program undergo change.

Premium quantities are determined by and paid to the life insurance policy vendor.

How can Universal Life Insurance protect my family?

If you retire after age 70, you might transform your GTLI protection to a private life insurance coverage plan (up to $200,000 optimum). Costs quantities are identified by and paid to the life insurance coverage supplier.

The benefit amount is based upon your years of employment in a qualified appointment at the time of retired life and is payable to your recipient(-ies) as follows: $2,000 $3,000 $4,000 $5,000 This is intended to be an introduction. Describe the Strategy File for total information. In the occasion the details on these pages differs from the Strategy Paper, the Strategy File will control.

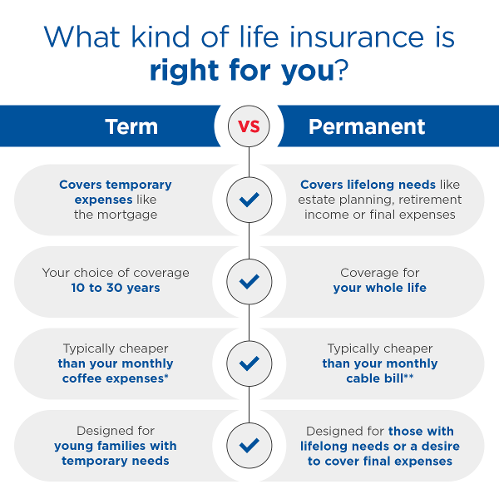

Term life insurance policy policies expire after a particular variety of years. Long-term life insurance policy plans continue to be energetic till the insured person dies, stops paying costs, or surrenders the policy. A life insurance policy plan is only like the financial toughness of the life insurance company that issues it. Investopedia/ Theresa Chiechi Various sorts of life insurance are readily available to fulfill all kind of customer demands and preferences.

Whole Life Insurance

Term life insurance coverage is developed to last a particular number of years, after that end. You choose the term when you secure the policy. Typical terms are 10, 20, or 30 years. The most effective term life insurance policy policies balance price with long-lasting economic toughness. Level term, the most usual kind of term insurance presently being offered, pays the very same quantity of death benefit throughout the policy's term.

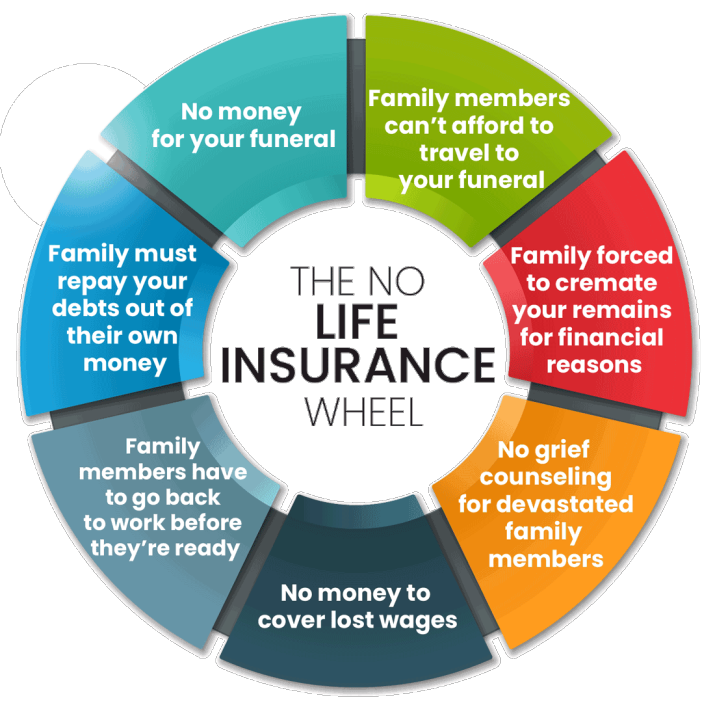

Overall what these costs would certainly more than the next 16 or two years, add a little extra for inflation, which's the fatality benefit you might intend to buyif you can afford it. Burial or last expense insurance coverage is a type of long-term life insurance that has a tiny death benefit.

What happens if I don’t have Wealth Transfer Plans?

Many factors can affect the expense of life insurance coverage costs. Particular points may be beyond your control, yet various other standards can be taken care of to potentially lower the price before (and also after) applying. Your wellness and age are one of the most important aspects that establish expense, so buying life insurance policy as quickly as you require it is frequently the finest program of action.

If you're found to be in far better wellness, then your premiums may reduce. You may also be able to get extra protection at a reduced rate than you initially did. Investopedia/ Lara Antal Consider what costs would certainly require to be covered in the event of your fatality. Think about things such as home loan, college tuition, charge card, and various other debts, not to state funeral expenditures.

There are valuable devices online to compute the lump amount that can satisfy any kind of potential expenditures that would need to be covered. Life insurance coverage applications usually require individual and family case history and beneficiary info. You might need to take a medical examination and will certainly require to reveal any preexisting clinical conditions, background of moving infractions, Drunk drivings, and any type of hazardous leisure activities (such as automobile racing or skydiving).

Since women statistically live much longer, they usually pay lower prices than males of the same age. An individual who smokes is at danger for numerous wellness concerns that could shorten life and rise risk-based premiums. Clinical tests for most plans include evaluating for health problems such as heart disease, diabetic issues, and cancer cells, plus related clinical metrics that can indicate health and wellness risks.: Unsafe professions and leisure activities can make costs a lot more expensive.

How do I get Protection Plans?

A background of moving violations or driving while intoxicated can substantially raise the expense of life insurance policy costs. Basic types of recognition will certainly additionally be required before a policy can be composed, such as your Social Protection card, driver's permit, or united state key. Once you've set up all of your essential info, you can collect several life insurance policy estimates from various companies based on your study.

Because life insurance policy costs are something you will likely pay month-to-month for decades, locating the plan that ideal fits your needs can conserve you an enormous quantity of cash. Our schedule of the best life insurance policy business can provide you a jump beginning on your study. It lists the companies we've found to be the best for various kinds of demands, based upon our research of nearly 100 providers.

Below are some of one of the most crucial attributes and protections supplied by life insurance policy plans. Many people make use of life insurance policy to offer money to beneficiaries that would certainly experience economic hardship upon the insured's fatality. for wealthy individuals, the tax benefits of life insurance, consisting of the tax-deferred development of money value, tax-free returns, and tax-free survivor benefit, can provide additional strategic possibilities.

It might be subject to estate taxes, yet that's why wealthy people sometimes acquire long-term life insurance policy within a trust. The trust aids them avoid inheritance tax and protect the worth of the estate for their successors. Tax obligation evasion is a law-abiding method for lessening one's tax obligation responsibility and should not be perplexed with tax evasion, which is prohibited.

Why should I have Riders?

Married or not, if the death of one grownup may mean that the other might no longer manage lending settlements, upkeep, and tax obligations on the residential property, life insurance coverage might be a great concept. One instance would be an involved pair that obtain a joint mortgage to purchase their initial residence.

This assistance might likewise include straight financial backing. Life insurance policy can assist repay the grown-up child's costs when the moms and dad dies - Living benefits. Young grownups without dependents rarely need life insurance policy, but if a moms and dad will be on the hook for a youngster's financial debt after their fatality, the youngster might intend to bring sufficient life insurance to pay off that debt

A 20-something adult may acquire a policy even without having dependents if they anticipate to have them in the future. Stay-at-home spouses should have life insurance as they contribute substantial economic worth based upon the work they do in the home. According to, the economic worth of a stay-at-home parent would be equal to a yearly wage of $184,820.

'A tiny life insurance policy policy can supply funds to honor an enjoyed one's death. If the fatality of an essential employee, such as a CEO, would create severe economic difficulty for a firm, that company may have an insurable rate of interest that will certainly permit it to purchase a key individual life insurance policy plan on that worker.

Who has the best customer service for Policyholders?

This technique is called pension plan maximization. such as cancer, diabetic issues, or smoking cigarettes. Note, however, that some insurance firms might reject protection for such people or fee very high rates. Each policy is unique to the insured and insurance company. It's vital to evaluate your plan record to understand what dangers your policy covers, how much it will pay your recipients, and under what conditions.

That stability issues, considered that your successors might not get the death benefit till lots of decades into the future. Investopedia has evaluated scores of companies that offer all various kinds of insurance and rated the ideal in numerous groups. Life insurance can be a sensible economic tool to hedge your wagers and supply security for your liked ones in situation you die while the policy is in force.

It's vital to consider a number of elements before making a choice. What expenditures could not be met if you died? If your partner has a high income and you do not have any children, maybe it's not necessitated. It is still vital to take into consideration the influence of your potential fatality on a partner and consider just how much monetary assistance they would certainly need to regret without stressing over returning to function before they prepare.

If you're getting a policy on one more relative's life, it is necessary to ask: what are you trying to guarantee? Children and seniors really don't have any purposeful income to change, yet funeral costs may require to be covered in case of their death. On top of that, a parent might intend to protect their youngster's future insurability by purchasing a moderate-sized policy while they are young.

What should I know before getting Estate Planning?

Term life insurance policy has both elements, while permanent and whole life insurance coverage plans likewise have a money value element. The fatality advantage or stated value is the quantity of cash the insurer assures to the beneficiaries recognized in the policy when the insured passes away. The guaranteed could be a moms and dad and the recipients might be their youngsters, for instance.

Costs are the cash the insurance holder pays for insurance.

{kind=link}

Table of Contents

- – What is the best Legacy Planning option?

- – What types of Living Benefits are available?

- – How long does Wealth Transfer Plans coverage ...

- – How can Universal Life Insurance protect my f...

- – Whole Life Insurance

- – What happens if I don’t have Wealth Transfer...

- – How do I get Protection Plans?

- – Why should I have Riders?

- – Who has the best customer service for Policy...

- – What should I know before getting Estate Pla...

Latest Posts

Instant Term Life Insurance Coverage

Average Cost Of Final Expense Insurance

Cremation Insurance

More

Latest Posts

Instant Term Life Insurance Coverage

Average Cost Of Final Expense Insurance

Cremation Insurance